Solar Energy Superbooms Sweep the Globe

Rest of World Set to Follow Vanguard Nations

Solar energy is the fastest growing source of energy in the history of the world, and is booming in nearly every country on Earth.

But in the past few years, some nations have been roiled by solar “superbooms” whose growth rates have far surpassed the global average. These superbooms have profoundly transformed these nations’ energy and emissions landscapes in a very short amount of time.

In this analysis, we define a superboom as any nation that has averaged at least a 2.5 percentage point gain in solar’s share of total electricity generation over either a three or five year period. At this growth rate, these nations would add a minimum of 25 percentage points to solar energy’s share over a ten-year period and 50 percentage points over a twenty-year period - a truly transformative level of growth.

There are twenty-two nations that currently fit this definition of a superboom, in addition to two US states (see above). The rapid growth of solar in every country is driven by rapidly falling prices of solar panels and batteries, largely made and exported by China. But there are three distinct reasons why these twenty-two nations have entered into a superboom state:

Group 1: Fossil Grid Collapse

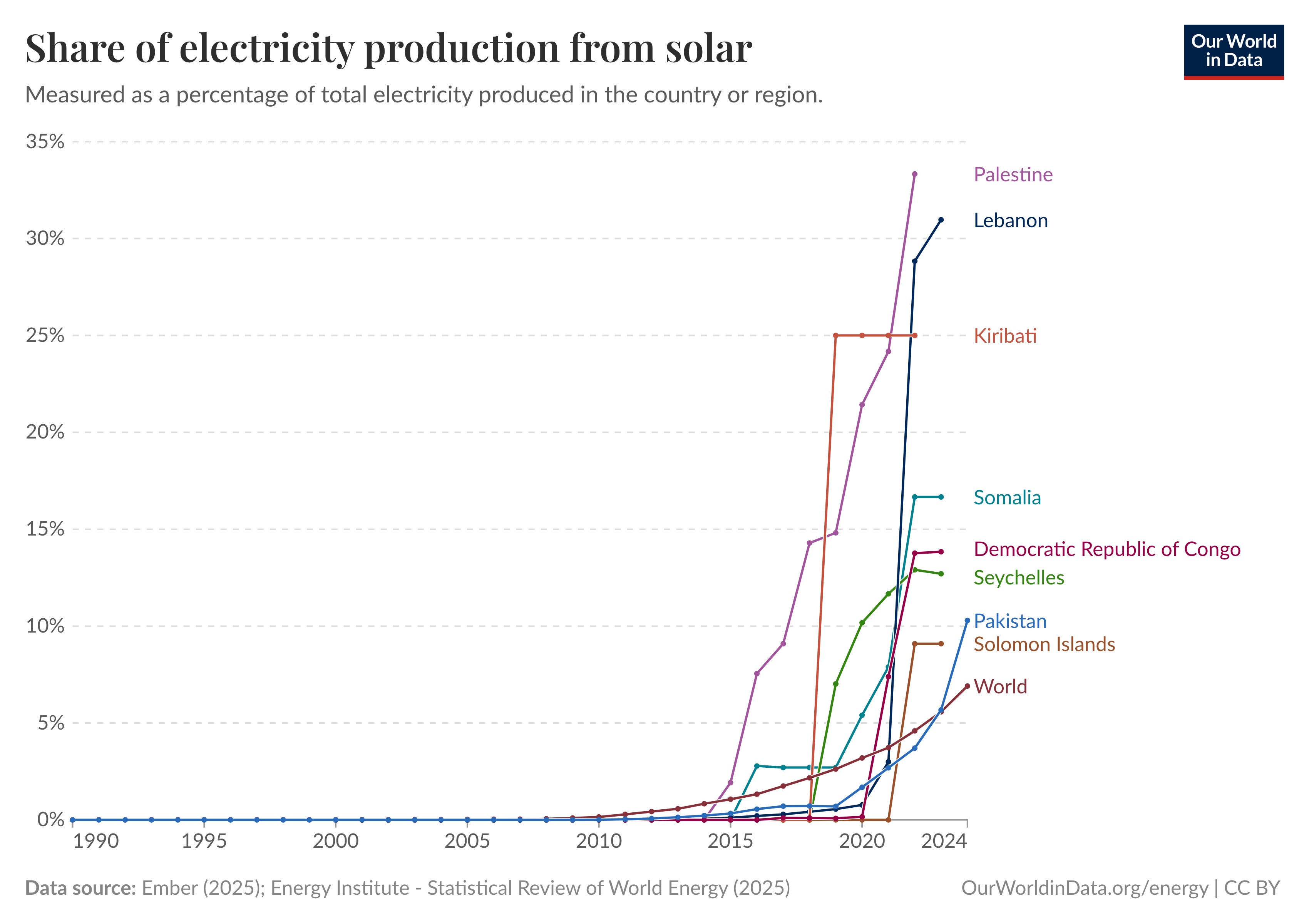

The largest solar booms anywhere in the world are occurring in places where the economic competitiveness of the fossil generation grid has collapsed due to conflict, remoteness, or mismanagement.

The single fastest solar adoption rate anywhere in the world has been in Lebanon. The cedar-draped Levantine nation has never had a particularly reliable grid, but recent economic troubles have worsened the situation. The grid typically provides power only a few hours a day, and households had previously relied on expensive diesel generators to fill the gap.1

Now they increasingly rely on solar. Solar’s share of Lebanon’s electricity generation has skyrocketed from nearly nothing in 2020 to almost one-third today, driven primarily by rooftop installations on homes and businesses, which use solar + storage to opt out of the failing fossil grid.

The situation is similar in nearby Palestine, where the Israeli occupation of the West Bank and the war in Gaza pose thorny and sometimes horrifying challenges. Prior to the Gaza War, Palestine was almost entirely dependent on Israel for electricity and fuel imports. Palestinian authorities encouraged solar farms and rooftop installations to gain some measure of energy sovereignty. 2

After the October 7th, 2022 attacks, Israel cut off fuel to Gaza, forcing its only fossil generation plant to go offline. Israel then destroyed most of Gaza’s electricity generation, transmission, and distribution infrastructure on the pretext that electricity could possibly be useful to Hamas. This destruction included the targeting of larger solar farms.

But solar energy’s modular nature means smaller photovoltaic installations still operate in Gaza, providing a vital lifeline to Gazan civilians who would otherwise be entirely without electricity.3 These small solar arrays allow hospitals, businesses and residences to provide a minimum level of functionality to civilians caught in a war zone.

The Gaza War has proven that solar is superior in conflict zones to a centralized grid, which can be bombed, or to diesel generators, which can be starved of fuel. And that lesson has been learned in the West Bank, whose residents are rapidly installing solar too.

Those lessons are also being applied in Congo (DRC), where social enterprise Nuru Energy is building solar + storage mini-grids in conflict zones to provide electricity to civilians. The company’s 1.3 MW facility in the contested city of Goma survived a rebel takeover earlier this year and powers 1700 households, 700 small businesses, and 600 other institutions.4

“Before, the only energy we had were diesel generators that weren’t powerful enough, didn’t always work, and were too expensive”, Norbert Kashemwa, director of a local school told Le Monde in 2023. “With Nuru, there are no more power cuts.”

Congo is one of the few nations in the world where a majority of people still lack access to electricity altogether, with an electrification rate of 22% in 2023. The problem isn’t so much generation - Congo has vast amounts of hydropower - but rather the expense of building transmission lines across a vast, heavily forested area the size of Western Europe. Solar mini-grids of the sort Nuru builds circumvent this problem by bringing generation directly to the people. It aims to extend its mini-grid systems to 10 million Congolese (~9% of the population) by 2030.

Solar mini-grids also explain the presence of small island nations like Kiribati and the Seychelles among the solar superboomers. Kiribati is a collection of 33 tiny islands scattered across 3.5 million km² (1.3 million mi²) of the Pacific Ocean. A centralized grid here would be impossible, so solar mini-grids are displacing dirty and expensive imported diesel generation.

The Seychelles faces similar challenges in the Indian Ocean, and is pursuing floating solar - placing solar panels in the sea - to spare more of its precious 457 km² (147 mi²) land area.5 The same technology has enormous potential elsewhere in the world, especially atop reservoirs.

By far the most consequential nation in this group is Pakistan. Although it ranks low on the 3-year average list, that’s only because its solar boom is so new. It was among the fastest-growing in 2024 and is the most populated of the superboomers with 240 million people.

Pakistan is devoid of fossil resources, its electricity grid is antiquated, and a few years ago it removed subsidies that once made electricity affordable. The result has been skyrocketing electric bills and households using cheap solar panels from China to opt out of a failing system.

And the cheap panels are just the beginning. The Pakistani market has been hugely innovative in reducing the soft costs associated with rooftop solar (i.e. labor, permitting, sales, etc). In Western countries, consumers pay thousands of dollars to have professional electricians install solar panels on their roofs. In Pakistan, people use TikTok and YouTube tutorials to do it themselves.6

The total installed cost of a residential solar installation in Pakistan is now between $290-$430 per kW, which is up to 50% cheaper than a comparable installation in Australia and over 80% cheaper than in the United States.78 Pakistan’s cost structure exposes the soft cost bloat in the developed world, but also illuminates the path for expansion of the solar superboom into the rest of the developing world, particularly Africa. If rural Pakistanis can afford rooftop solar, anyone can.

Group 2: Sunniest Places on Earth

Solar photovoltaic energy works anywhere, as no place on Earth lies in complete darkness 24 hours a day, 365 days a year. But it is certainly more economic in places with higher levels of sunlight. The second group of solar superboomers are geopolitically stable, sunny places with enormous solar resources and supportive government policy.

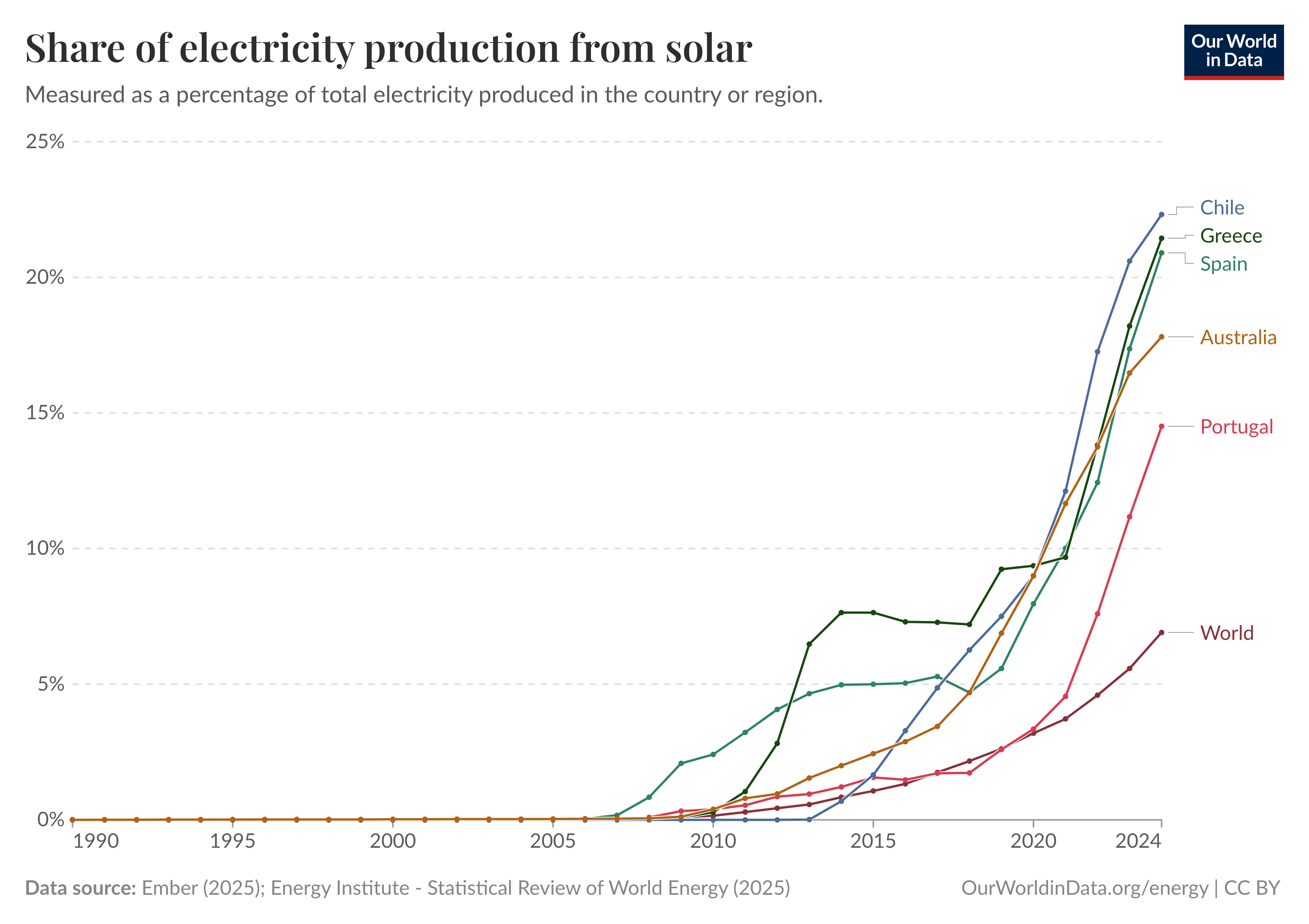

Foremost in this group is Chile, whose Atacama Desert is one of the sunniest places on Earth. The Atacama is extremely dry, with an average rainfall of only 15 mm (0.6 in) a year. It sits at a high elevation, meaning there is less atmospheric interference between the panels and the sun. It is in the Southern Hemisphere, which gets slightly more sun than the Northern Hemisphere due to Earth’s elliptical orbit. And it is cooler than most deserts, improving the conversion efficiency of solar panels. All of this makes the Atacama the single best place on Earth for solar energy.

Solar has rocketed from nearly nothing in 2014 to 22.3% of Chile’s electricity generation last year. Already Chilean policymakers are thinking about how to export their uniquely abundant solar resource to the rest of the world.

The leading idea is the low-carbon manufacture of liquid fuels such as hydrogen, ammonia, methanol or synthetic hydrocarbons for use in the shipping and aviation industries. These fuels can be made using electricity, and Chilean solar will be among the cheapest electricity anywhere in the world. One day aircraft all over the world may be powered by low-carbon jet fuel synthesized using solar farms in the Atacama.

The Southern Hemisphere has more than one solar overachiever. Australia was nicknamed “the lucky country” because of its immense resources of coal, iron, copper, gold and other minerals relative to its small population - a ratio that has undergirded the nation’s prosperity since its founding during the Industrial Revolution. Remarkably, it is equally blessed with energy transition resources, with extremely high solar irradiance per capita.

Australia’s solar revolution is double-barreled, relying on both rooftop and utility-scale projects, with utility-scale accounting for 10% of the country’s electricity generation in the first half of 2025 and rooftop providing an additional 12.8%.9 Fully one-third of Australian homes now have solar panels on their roofs, the highest figure in the world.10

The state of South Australia has been the leader in renewable energy. In 2024, solar generated 29% of South Australia’s electricity, with wind accounting for 45.3%. This extremely high penetration of variable renewable resources definitively debunks the myth that large electricity grids cannot cope with wind and solar generation.11

These load-balancing challenges are also being met in the United States, where solar has reached nearly a third of electricity generation in the sunny states of Nevada and California. The solution has been first and foremost to pair solar projects with massive amounts of storage.

Group 3: Serious Policy Support

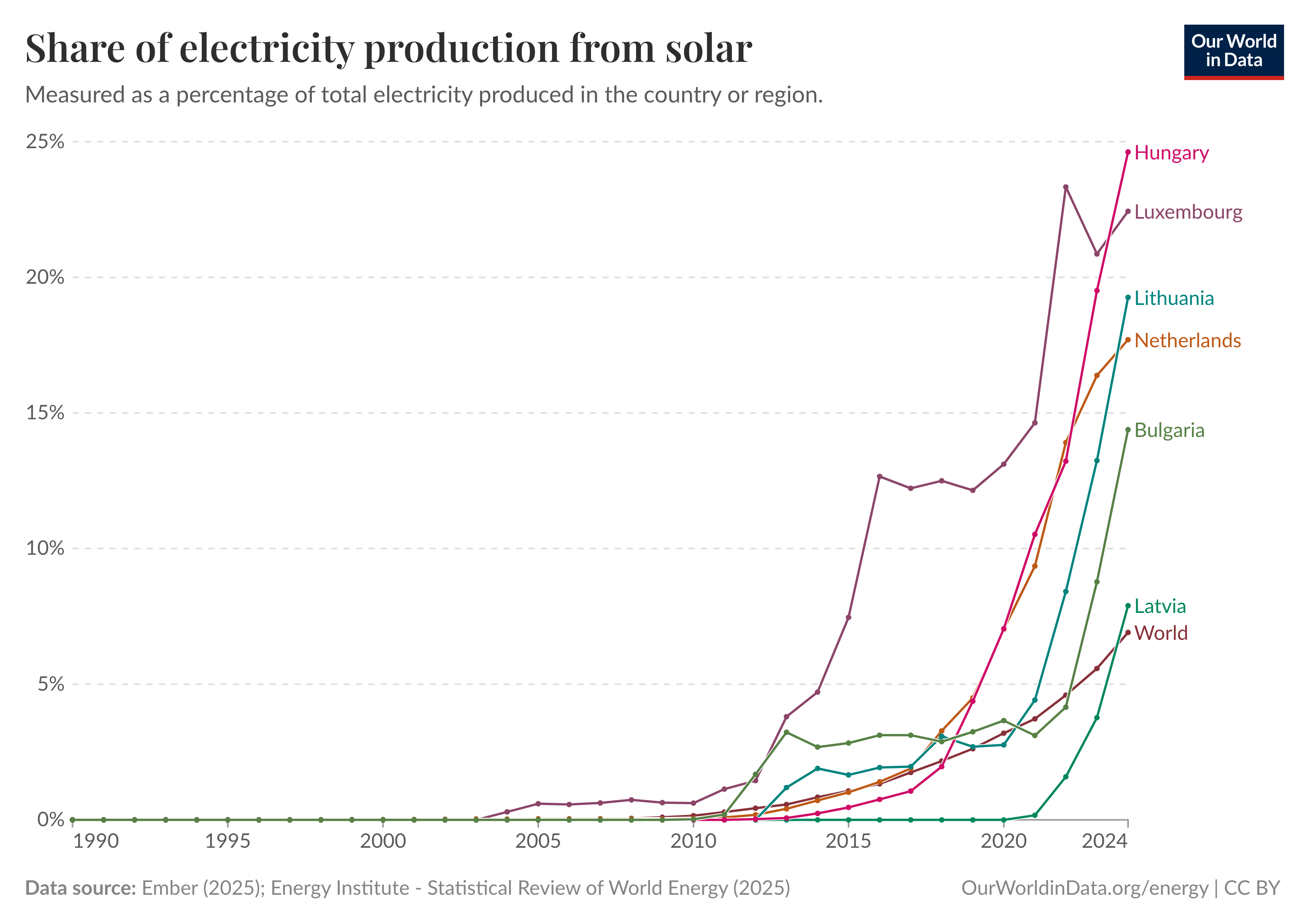

The third group of solar superboomers are countries that do not have excellent solar resources, but do have generous subsidy regimes which promote solar to meet climate or energy security goals. A leader in this group is the Netherlands, which has managed to successfully engineer a solar boom despite being significantly cloudier and at higher-latitudes than nearly any other country listed.

Solar energy is often slandered with the charge of being too “land intensive” relative to competing technologies like fossil fuels and nuclear. In truth, land is typically not a constraint on utility-scale ground-mounted solar development except in a few places - like the Netherlands, Singapore or Bangladesh- where very high population densities make land scarce.

But even in places where ground-mounting is difficult, there are always rooftops. 60% of solar capacity in the Netherlands is on commercial rooftops, with another 30% coming from homes and only 10% from utility-scale solar farms.12 This capacity is supported by very generous government subsidies, including a net-metering scheme, 0% sales tax on solar panels, and low interest loans on solar systems. Together, these subsidies can offset between 40%-60% of total system cost.13

Hungary is perhaps a surprising name in this group. It is not particularly sunny and is governed by a long-serving, populist, right-wing government of the sort that - in the Anglophone world - would gleefully oppose renewable energy. But Hungary lacks fossil fuel resources of any kind and its energy security strategy has been to go all-in on the only two homegrown options available - nuclear and solar.

The nuclear component of this strategy is in trouble, as Hungary mistakenly chose a Russian reactor design to replace its existing Soviet-era generation - a deal now imperiled by sanctions.14 But solar is roaring. The country has the highest percentage of solar energy in Europe, backed by ample subsidies similar to those in the Netherlands.

In the United States, the northeastern state of Maine has taken a unique subsidy strategy, honing in on community solar - medium-sized grid-tied projects large enough to power neighborhoods. These sorts of installations can be more economically efficient than residential rooftop, and make up about a third of Maine’s solar capacity.

Tomorrow, The World

The success of solar energy in such a diverse set of countries highlights the decisive advantage of its modular nature, which allows the technology to be shaped and adapted to local needs. Solar panels can be configured as massive multi-GW solar farms in Chilean or Nevadan deserts, modest community solar in Maine, mini-grids in Africa and the Pacific, commercial rooftop installations in Europe, or residential micro-generators in Australia. And it all works.

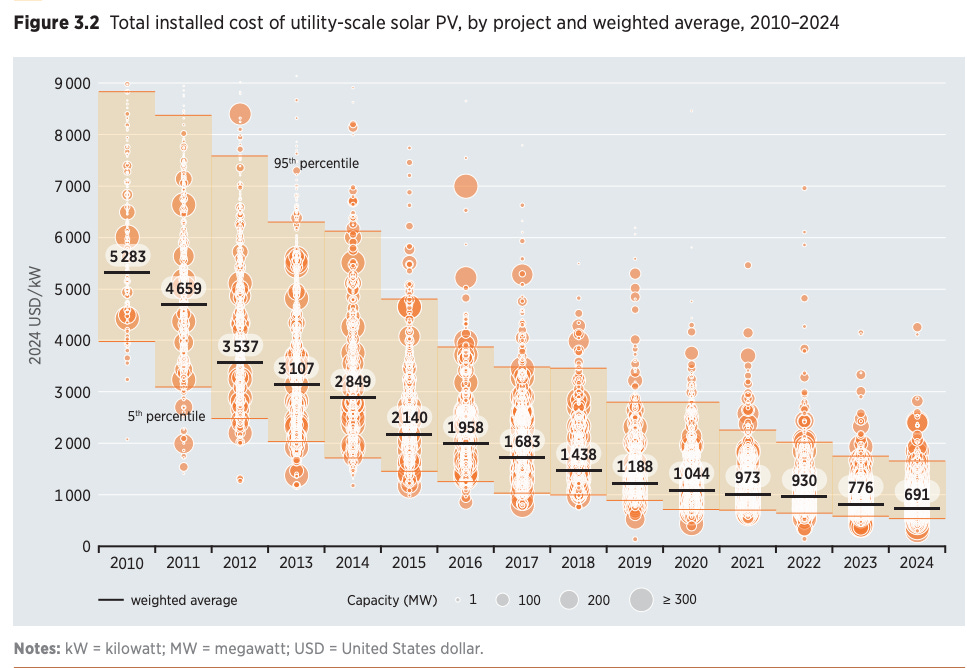

Solar panels are mass-produced manufactured products, and as such they benefit from economies of scale to a greater degree than fossil fuels or nuclear. The installed cost of a utility-scale solar plant has declined 87% since 2010 and 34% since 2020 (see chart) and are projected to decline further.

Due to geographic and policy differences, the solar superboom took off first in the twenty-two countries listed above. But as solar energy gets cheaper, its economic competitiveness relative to fossil fuels will cross the superboom threshold in more places. Today, it’s Australia, Spain and Pakistan. Soon it will be Indonesia, the UK, and India. In the United States, places like Nevada, California, and Maine will be joined shortly by the likes of Kansas, New York, and Oregon.

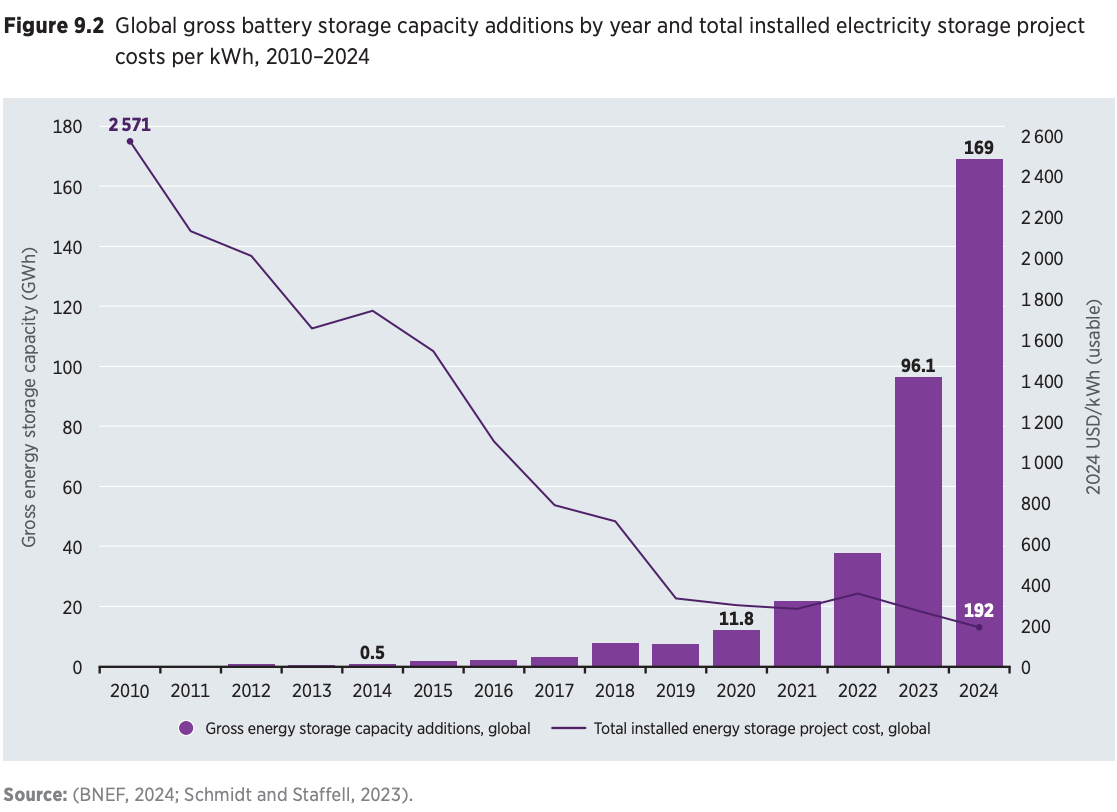

Assisting in the next phase of the solar energy revolution will be the plummeting cost of energy storage. Battery prices have fallen by 93% since 2010, and will continue to fall further as Chinese manufacturers scale the less expensive lithium-iron-phosphate (LFP) technology and introduce potentially even lower-cost chemistries like sodium-ion.

Batteries improve the economic competitiveness of solar projects by allowing them to time shift their generation and dispatch capacity to the grid when the sun isn’t shining. Solar + storage installations producing 24/7 electricity at prices competitive with fossil fuels are rare today, but they will become increasingly common in the next few years.15 Solar + storage projects have three cost components: the photovoltaic system itself, the battery and the soft costs. In most places, all three are falling precipitously.

It is extremely likely that in the next five years the entire world will enter into a solar superboom phase, in which the rate of solar growth ticks upwards - above the 2.5 annual percentage point level. Early indications in 2025 suggest the superboom is already extending across Africa, where most nations share the expensive, unreliable fossil grids of Group 1 countries.16 China may also cross into superboom territory next year.

This acceleration of solar deployment will make meeting climate goals much easier. Other sources of low-carbon electricity generation are stalling. Hydro is mostly tapped out. The much-promised nuclear renaissance has not happened, and will probably never happen. Wind energy is still growing, but not fast enough to meet the world’s growing demand for electricity.

Solar - however - is just getting started.